The Complete Financial Roadmap for US-Based NRIs

For US-based NRIs, financial planning is not merely about investing in India. It is about navigating two parallel legal systems, two tax jurisdictions, and two regulatory frameworks — each operating independently, yet affecting the same pool of capital.

Every transaction — whether it is opening a bank account, investing in equities, purchasing property, or contributing to retirement vehicles — must be evaluated from both an Indian and an American perspective.

This guide from FirstSource.pro brings together the structural, regulatory, and tax dimensions that every US NRI must understand before allocating capital to India.

The Foundation: Structuring Bank Accounts Correctly

Before discussing investments, the first layer of compliance begins with bank accounts. The structure you choose determines taxation, repatriation flexibility, and regulatory ease.

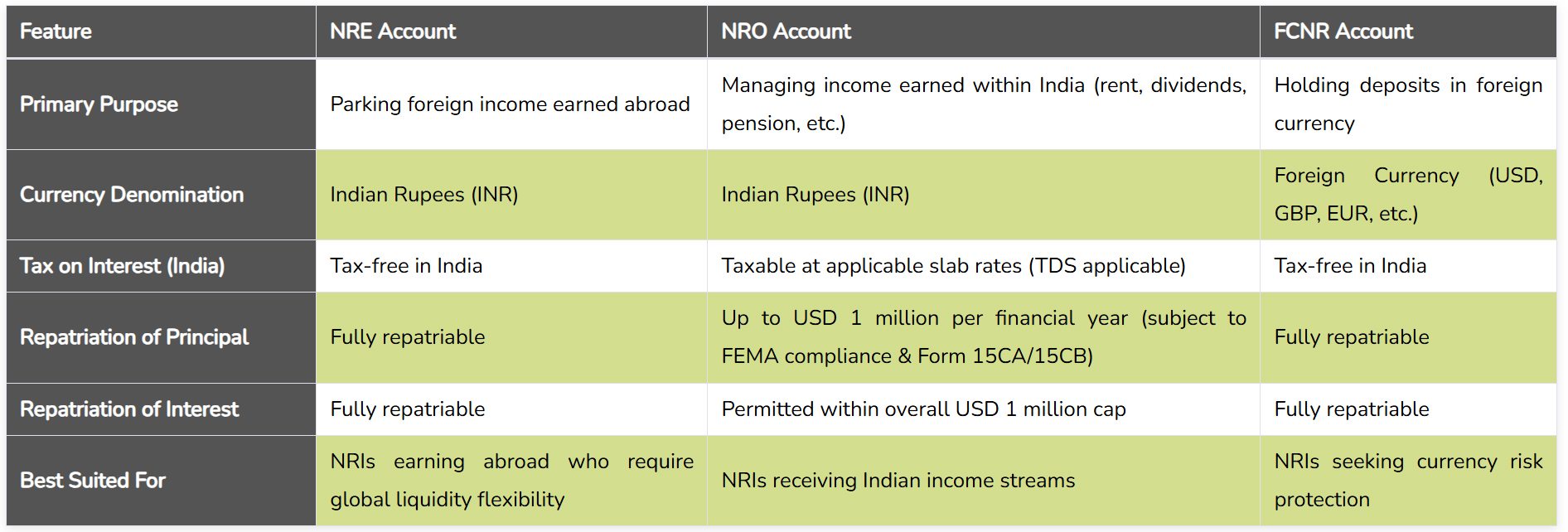

US-based NRIs typically operate through three types of accounts: NRE, NRO, and FCNR.

An NRE (Non-Resident External) account is designed to park income earned outside India. Funds deposited are converted into INR, and importantly, both the principal and interest are fully repatriable. Interest earned in this account is tax-free in India. For NRIs whose primary income originates abroad and who wish to maintain repatriation flexibility, the NRE account serves as the backbone of financial structuring.

The NRO (Non-Resident Ordinary) account, on the other hand, is meant to manage income generated within India — rental income, dividends, pension receipts, or business proceeds. Interest earned in an NRO account is taxable in India at applicable slab rates, and banks deduct TDS accordingly. Repatriation is permitted but capped at USD 1 million per financial year under FEMA regulations, subject to compliance with Form 15CA and 15CB certification by a Chartered Accountant.

The FCNR (Foreign Currency Non-Resident) account allows deposits to be maintained in foreign currency. This structure protects against currency fluctuation risk because the deposit is not converted into INR. Interest earned is tax-free in India, and both principal and interest are freely repatriable.

The distinction between these accounts is not cosmetic. It directly impacts liquidity planning, tax liability, and cross-border transfers. Many compliance complications faced by NRIs originate not from investments, but from incorrectly structured banking arrangements.

Direct Equity Investing: Understanding PIS and Non-PIS Routes

Once the banking foundation is established, the next question is how to access Indian equities.

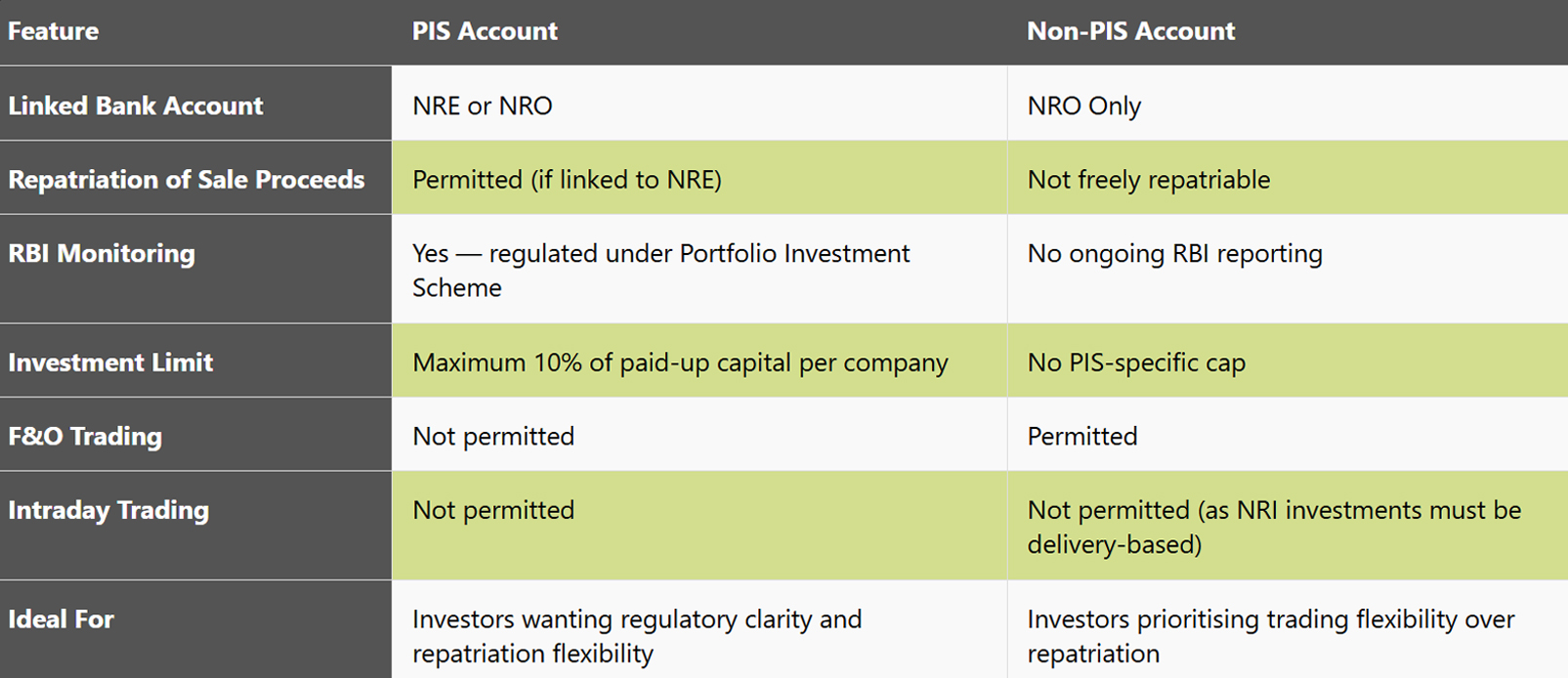

RBI regulations require NRIs to invest in listed equities either through the Portfolio Investment Scheme (PIS) route or through a Non-PIS structure.

A PIS account is specifically designed for regulated equity participation by NRIs. It can be linked to either an NRE or an NRO account. When linked to an NRE account, sale proceeds are repatriable. This makes it suitable for investors who may wish to move funds back overseas in the future.

However, PIS accounts are subject to RBI monitoring and come with specific limitations. NRIs cannot invest more than 10 percent of a company’s paid-up capital in specified shares. Additionally, intraday trading and derivatives (F&O) trading are not permitted under PIS.

A Non-PIS account, typically linked to an NRO account, offers greater operational flexibility. It allows participation in derivatives trading. Intraday trading is not permitted as NRI investments must be delivery-based. However, funds are not freely repatriable. This structure suits investors who intend to retain capital within India rather than move it abroad.

The choice between PIS and Non-PIS should not be made casually. It must align with long-term capital mobility plans and tax strategy.

Mutual Funds: Accessibility vs Tax Complexity

At first glance, Indian mutual funds appear to be a convenient investment avenue. However, for US-based NRIs, the situation is layered.

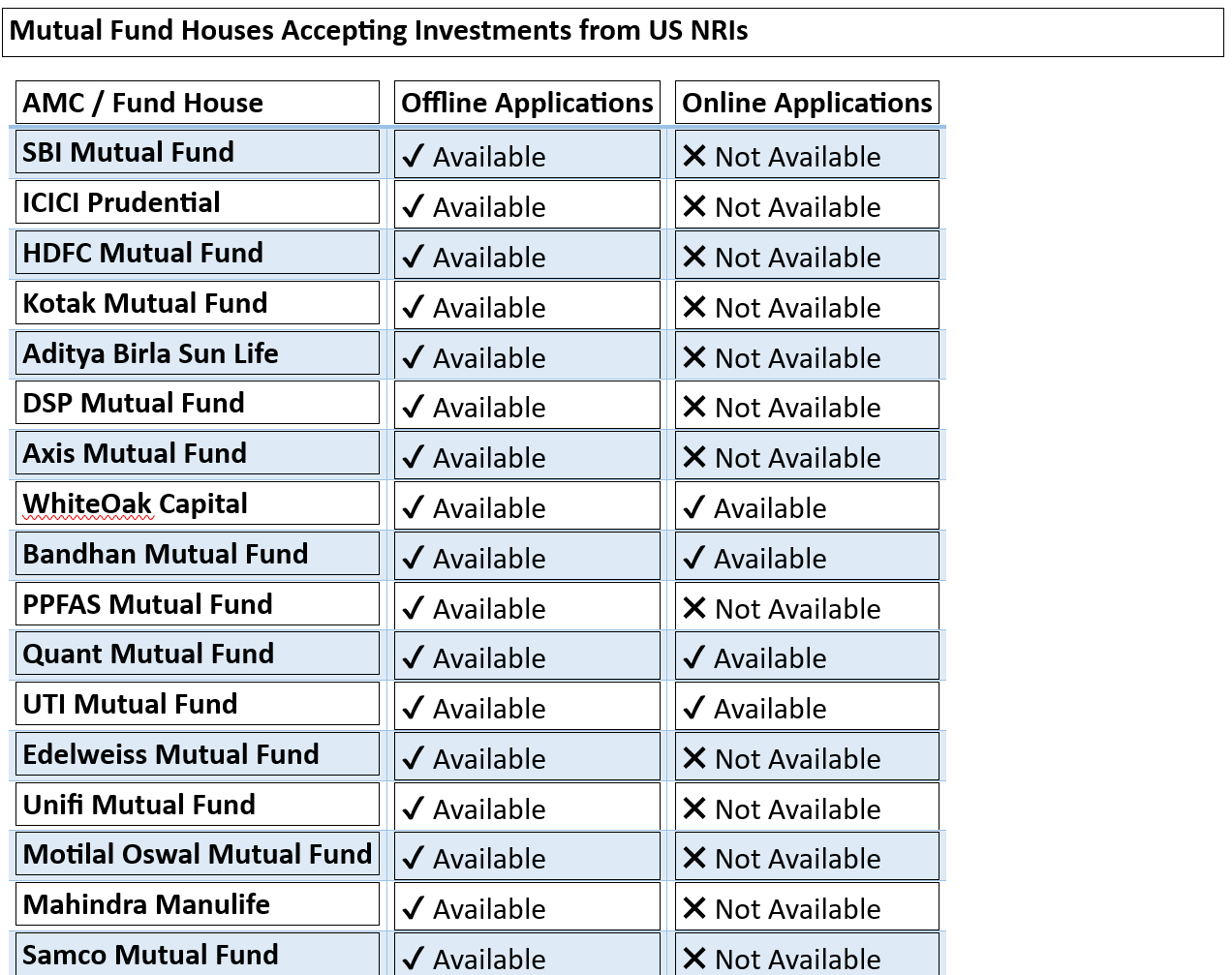

Several Indian fund houses accept investments from US NRIs, but often through restricted channels. Many require offline applications, requiring physical presence of the investor in India, and additional FATCA declarations. While digital access is slowly expanding, the process remains more compliance-heavy than for resident investors.

From an Indian tax standpoint, mutual funds are taxed at redemption. Equity mutual funds attract long-term capital gains tax @12.5% for gains above Rs. 1.25 lacs if held beyond twelve months and short-term tax @20% if sold earlier. Debt mutual funds are taxed at slab rates irrespective of holding period. TDS is deducted at source before redemption proceeds are credited.

However, the Indian tax treatment is only half the picture.

Important Notes for US-Based NRIs

- Offline applications typically require physical presence in India at the time of investment.

- A US FATCA declaration form must be submitted along with the application.

- TDS is deducted at source upon redemption.

- Availability of online mode may change based on AMC compliance policies.

The PFIC Layer: The Real US Tax Challenge

Under US tax law, most non-US pooled investment vehicles — including Indian mutual funds — are classified as Passive Foreign Investment Companies (PFICs).

PFIC classification significantly complicates taxation for US taxpayers.

Instead of being taxed only at redemption, gains may be subject to punitive taxation under PFIC rules, including mark-to-market taxation (if elected) or excess distribution treatment, even if units are not sold. Additionally, IRS reporting requirements (Form 8621) add compliance costs and complexity.

This results in two primary consequences:

- Accelerated tax liability compared to Indian rules

- Higher compliance burden and potentially punitive tax treatment

Although foreign tax credits may mitigate double taxation, the administrative complexity often leads many US NRIs to reconsider mutual fund exposure.

This is one of the most misunderstood aspects of cross-border investing.

K-1 Structures: A Structural Response to PFIC Complexity

One of the most sophisticated ways to address PFIC exposure for US-based investors is through the use of US partnership feeder structures that issue Schedule K-1.

To understand why this matters, it is important to first recognize the problem PFIC creates. When a US taxpayer directly invests in an Indian mutual fund, that fund is typically classified as a Passive Foreign Investment Company. The tax treatment becomes complex, reporting requirements increase, and long-term capital gains treatment may not apply in the way investors expect.

A K-1 structure approaches the same economic exposure differently.

Instead of the investor directly holding units of a foreign fund, the investment is routed through a US-domiciled partnership — typically structured as an LLC or Limited Partnership. This US entity then invests into an IFSC (GIFT City) vehicle or offshore feeder structure that provides exposure to Indian markets.

From a US tax perspective, the investor is no longer holding a PFIC. They are holding an interest in a US partnership.

That distinction is powerful.

Under US partnership rules, income, gains, losses, and credits “flow through” to investors. Each year, the partnership issues a Schedule K-1 that clearly reports the investor’s share of income. The investor includes this information in their personal tax return, just as they would with any domestic partnership investment.

The taxation becomes annual and transparent. There is no punitive excess distribution calculation. There is no mark-to-market election complexity. In most properly structured cases, Form 8621 reporting at the investor level is avoided.

Yes, taxes are paid annually on allocated income, even if distributions are not made. But that annual reporting follows a predictable and well-understood US framework.

That predictability is what makes the structure powerful.

The Practical Impact on Compliance

For many US NRIs, the frustration with PFIC is not just taxation — it is compliance friction.

Each PFIC investment can require separate Form 8621 filings. Over time, especially with SIP-style investing across multiple funds, the reporting becomes layered and expensive. Many US CPAs charge additional fees per PFIC filing due to the time and complexity involved.

With a K-1 structure, reporting consolidates into a single annual statement from the partnership. The investor’s CPA handles it within the standard partnership reporting framework.

This does not eliminate taxation. It eliminates uncertainty.

And for serious investors, uncertainty is more damaging than tax.

GIFT City: India’s Structural Bridge to Global Capital

For decades, non-resident investors accessed India through frameworks originally designed for resident investors. NRE and NRO accounts were created to manage currency flows. PIS structures were designed to monitor equity ownership. Domestic mutual funds were built under Indian regulatory assumptions.

GIFT City changes that architecture.

India’s International Financial Services Centre (IFSC), located at GIFT City in Gujarat, was conceptualized as a global financial hub operating under a distinct regulatory ecosystem. It is governed by the International Financial Services Centres Authority (IFSCA), a unified regulator created to align India’s financial infrastructure with international standards.

Unlike traditional domestic channels, IFSC structures are designed specifically for cross-border capital.

This distinction is critical for US-based NRIs and OCIs.

It allows foreign currency investments, structured feeder vehicles, and potentially smoother capital mobility. Several fund houses have launched IFSC-based funds with varying ticket sizes and structures.

While the ecosystem is evolving and minimum investment thresholds can be high, GIFT City represents an important structural development in India’s financial architecture for global investors.

What Makes GIFT City Structurally Different?

The first structural difference lies in currency flexibility. Investments in GIFT City can be made and held in foreign currency, typically USD. This eliminates unnecessary currency conversion layers that are otherwise embedded in NRE/NRO-linked investments.

Second, capital mobility is significantly smoother. IFSC structures are designed to be freely repatriable, aligning more closely with global investing norms rather than domestic capital control frameworks.

Third, the compliance environment is intentionally streamlined for global investors. In many cases, investment into IFSC funds does not require PAN or Aadhaar. Passport-based KYC is often sufficient. Certain structures also eliminate routine Indian tax filing obligations, depending on how the investment is set up.

But the most important shift is tax architecture.

Why GIFT City Matters for US-Based Investors

The biggest friction point for US NRIs investing in India has historically been PFIC classification of domestic mutual funds.

GIFT City creates the possibility of restructuring exposure.

Through properly designed feeder vehicles — particularly US partnership structures issuing Schedule K-1 — investors can gain exposure to Indian markets without directly triggering PFIC complications. This does not eliminate taxation. It reorganizes it under a more predictable US framework.

In effect, GIFT City enables alignment between Indian growth opportunities and US tax efficiency.

This is not merely regulatory convenience. It is structural modernization.

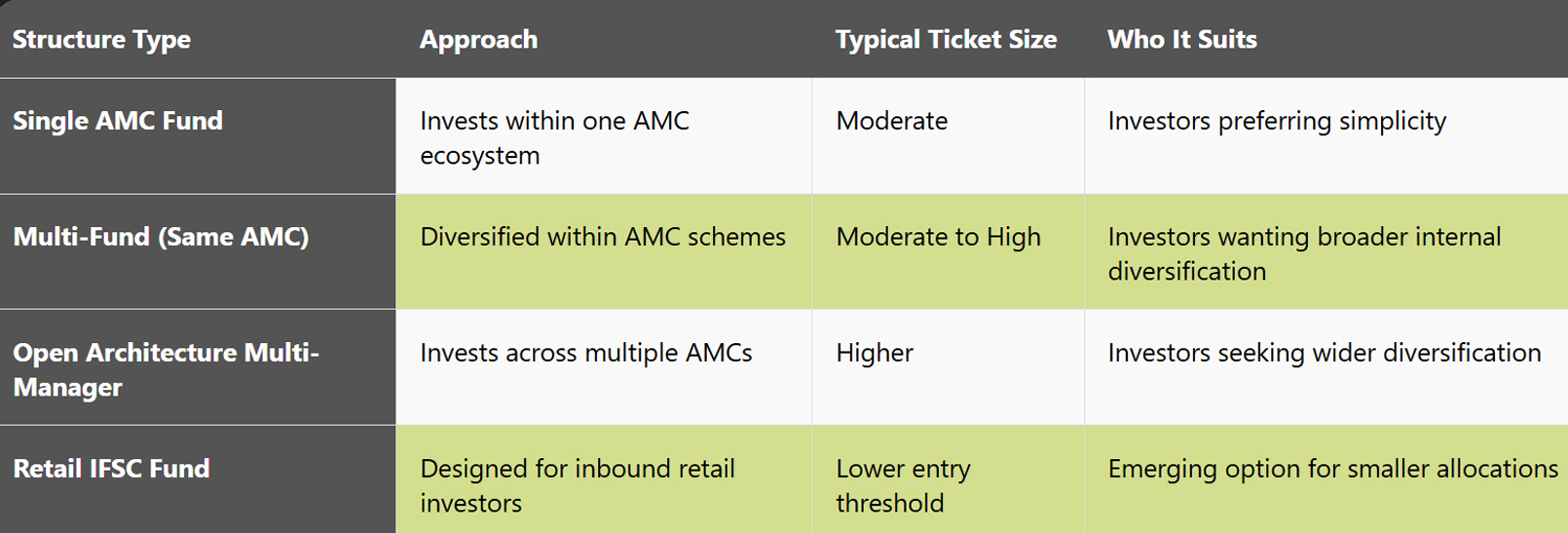

Evolution of IFSC Funds

Initially, IFSC funds catered primarily to large-ticket investors. Minimum investment thresholds were high, and access was limited to sophisticated capital.

That landscape is evolving.

Single-AMC structures, multi-manager funds, open-architecture models, and retail-oriented inbound funds are gradually expanding the spectrum of participation. As product innovation increases and regulatory clarity deepens, the ecosystem is becoming more inclusive while retaining institutional rigor.

For US-based investors, this evolution matters. It signals that GIFT City is not a niche experiment — it is a long-term strategic platform.

The Bigger Strategic Picture

India is one of the fastest-growing major economies in the world. Global capital wants exposure. The challenge has always been integration — aligning Indian opportunity with international legal and tax frameworks.

GIFT City represents India’s answer to that challenge.

Over the coming decade, as IFSC infrastructure matures, K-1 integrated feeder structures expand, and global custodial systems integrate more seamlessly, GIFT City is likely to become the preferred route for serious cross-border investors.

For US NRIs and OCIs, this is particularly significant.

Traditional domestic routes were functional but friction-heavy. IFSC structures are globally aligned from inception.

The future of NRI investing in India will not be defined only by returns. It will be defined by efficiency, transparency, and structural harmony between jurisdictions.

And GIFT City sits precisely at that intersection.

List of K-1 Compliant GIFT City Funds

How K-1 Structure Helps (Illustrative Example)

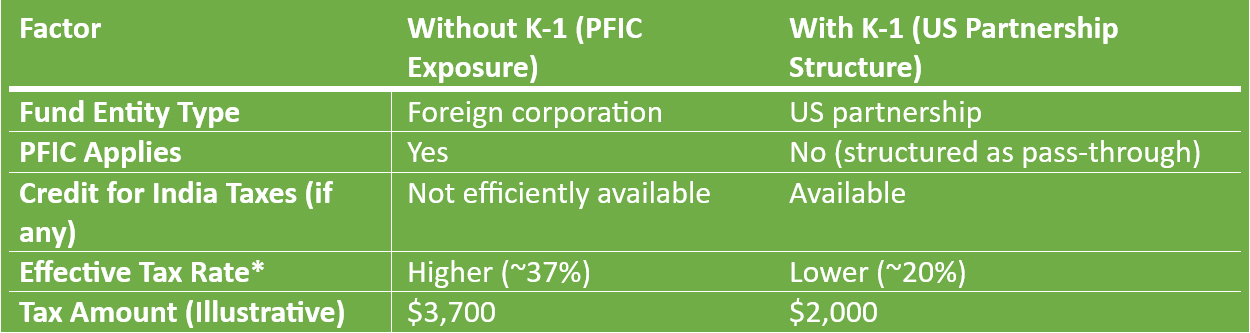

Example: A US-based NRI invests $100,000 in a GIFT City fund.

Assumed tax figures for illustration. Without a K-1 structure, US NRIs may face PFIC taxation, where unrealized gains can be treated as ordinary income and taxed at rates up to 37%. Actual tax rates may vary based on individual tax profile, holding period, and applicable US tax elections.

Real Estate: TDS and Capital Gains Nuances

Real estate continues to be a preferred asset class for many NRIs. However, taxation rules differ significantly from resident transactions.

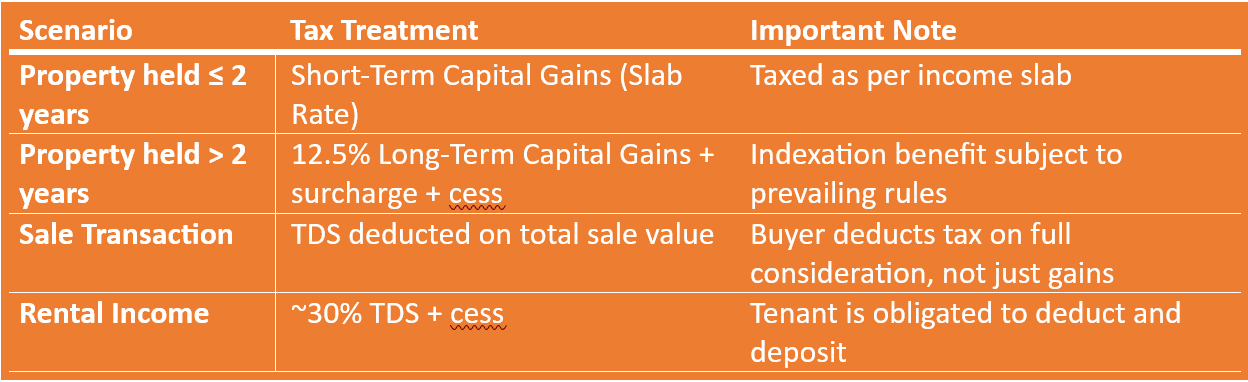

If property is held for more than two years, gains qualify as long-term capital gains and are taxed at 12.5 percent plus surcharge and cess. If sold within two years, gains are treated as short-term and taxed at slab rates.

The greater challenge lies in TDS deduction mechanics.

When an NRI sells property, the buyer is required to deduct TDS on the entire sale value — not merely on the capital gain component. This often results in excess deduction. To mitigate this, NRIs must proactively apply for a lower TDS certificate under Form 13.

Rental income is subject to approximately 30 percent TDS. Tenants are legally obligated to deduct and deposit this amount. Rental agreements can be executed via physical presence, Power of Attorney, or Aadhaar-enabled digital signature.

Additionally, NRIs are not permitted to purchase agricultural land in India, though inheritance is allowed.

EPF, PPF, and NPS: Retirement Structures

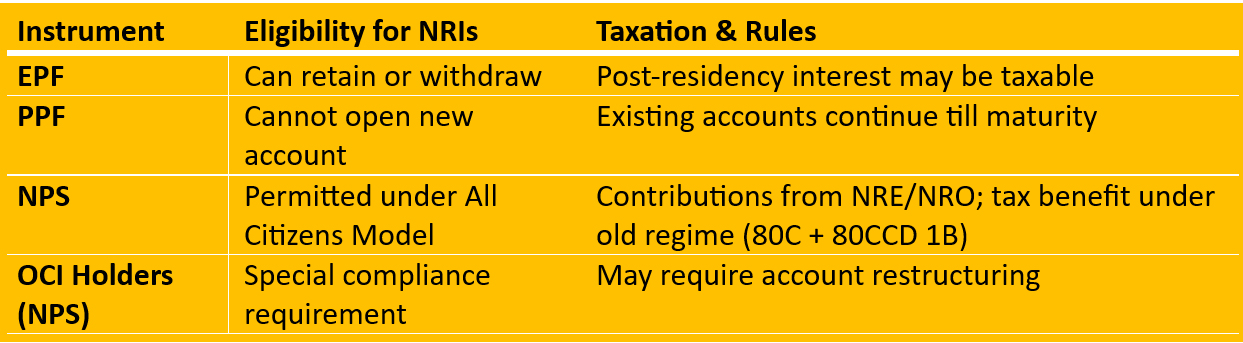

Employee Provident Fund balances accumulated during Indian employment may remain invested, but interest accrual post change in residential status may be taxable.

Public Provident Fund accounts cannot be opened by NRIs after residency change. However, accounts opened prior to becoming non-resident can continue until maturity.

The National Pension System (NPS) remains accessible to NRIs under the All Citizens Model. Contributions must originate from NRE or NRO accounts. Tax benefits under Sections 80C and 80CCD(1B) remain available if filing under the old regime in India.

OCI holders must note that regulatory treatment differs and may require structural adjustments.

Estate Tax Considerations

US estate tax exposure for non-resident aliens can apply at low thresholds for US situs assets. This dimension is often overlooked in NRI planning but must be integrated into long-term wealth structuring.

Closing Perspective: Integration Is the Real Strategy

For US-based NRIs, wealth creation in India cannot be evaluated in isolation.

Every financial decision must pass through multiple filters:

- Is this compliant under FEMA?

- How will this be taxed in India?

- How will it be taxed in the United States?

- Does this create PFIC exposure?

- Is capital freely repatriable?

- What are the estate and succession implications?

The objective is not merely investing in India.

The objective is building a cross-border structure that is efficient, compliant, and sustainable over decades.

And this is precisely where GIFT City becomes strategically relevant. While the ecosystem is still evolving, the direction is unmistakable.